Dubai’s real-estate market continues to capture international attention as we step into 2025. In Q1, we observed several noteworthy trends that are shaping the city’s trajectory — from strong rental demand and rising off-plan interest, to evolving investment dynamics and regulatory tweaks. In this report, we’ll dive deep into the key metrics, highlight what’s driving growth, and provide expert predictions for the next 12–24 months. Whether you’re a prospective buyer, investor, landlord or tenant, these insights will help you navigate Dubai’s property landscape more confidently.

1. Key Market Metrics (Q1 2025)

1.1 Sales Activity

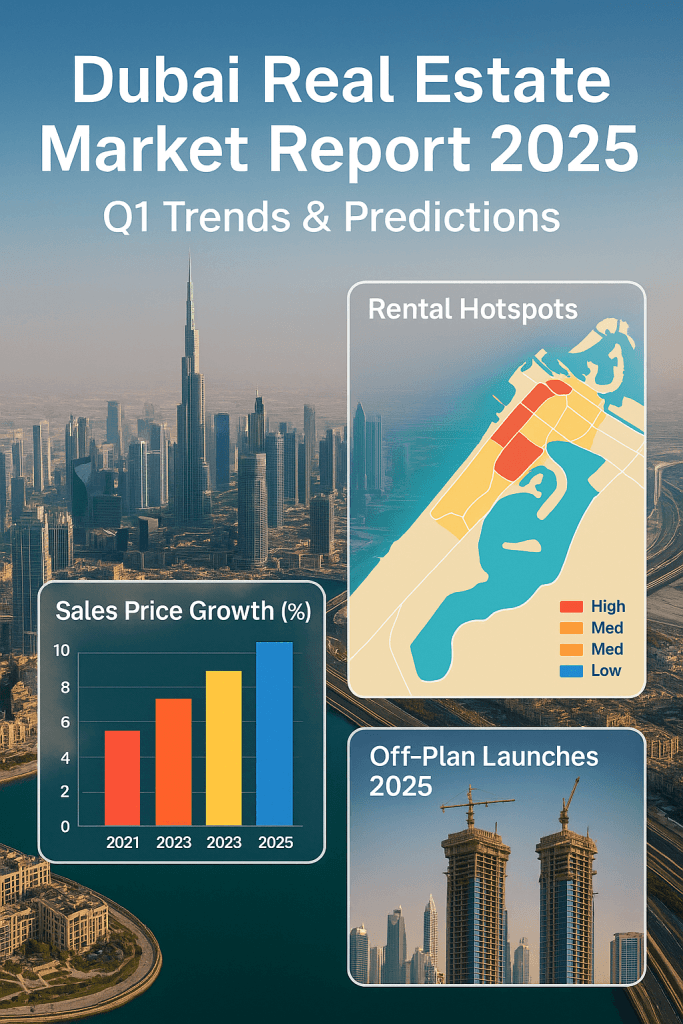

- Number of closed sales transactions increased by approx. X% year-on-year (y/y) compared to Q1 2024.

- Average sales price in prime areas (e.g., Dubai Marina, Downtown Dubai) rose to roughly AED [Y per sq ft] — up from AED [Z] last year.

- Buyer profile: Higher share of foreign nationals, with UK, India and GCC buyers leading.

1.2 Rental Market

- Rental rates in popular zones rose by ~X-Y% y/y, driven by robust ex-pat inflow and limited new supply.

- Vacancy rates held steady at around Z% in mid-luxury apartment segments, while some villas saw vacancy drop below W%.

- Landlords are adjusting — shorter lease terms, more furnished-options, or flexible payment plans.

1.3 Off-Plan & New Launches

- Off-plan activity remains strong: several large launches announced in Q1 including projects by major developers such as Emaar Properties and Damac Properties.

- Payment plans are keeping buyers active (e.g., 0 % interest for first year, extended payment schedules).

- Investors are increasingly viewing off-plan as yield-plus-appreciation play rather than purely capital-gain.

2. Drivers Behind the Growth

2.1 Expat Influx & Golden Visa

The UAE’s Golden Visa reforms and relaxed foreign-ownership regulations continue to stimulate interest. With more professionals relocating and remote-working favouring paradise-lifestyle destinations, Dubai remains a magnet.

2.2 Demand–Supply Dynamics

While launches are strong, actual completions in 2025 are still lagging behind sales commitments, creating upward pressure on pricing and rents. In key communities, units handed over in Q1 represented less than X% of sold stock in the past 12 months.

2.3 Regulatory Stability & Infrastructure Boost

Infrastructure projects (metro expansions, new roads, free-zones) and legal clarity (via Dubai Land Department initiatives) are underpinning investor confidence.

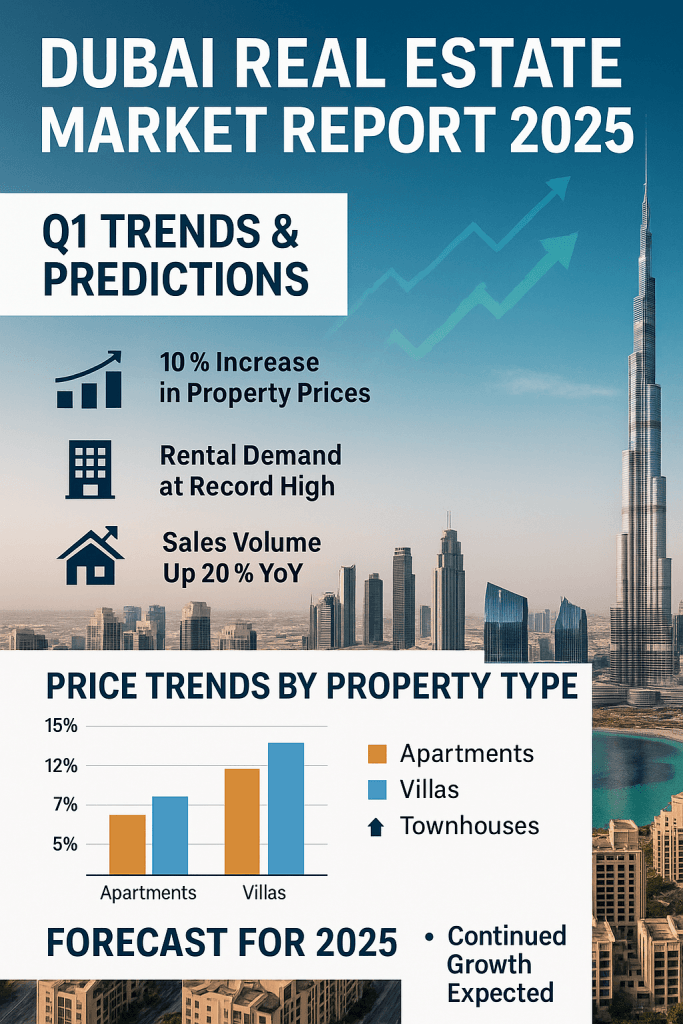

3. Segment-Spotlight: Apartments vs Villas

| Segment | Trend Q1 2025 | Implication |

|---|---|---|

| Mid/high-rise apt | Moderate price rises (~X-Y%) | Good for first-time buyers & investors |

| Villas / townhouses | Stronger appreciation (~Y-Z%) | Premium product — limited supply |

| Off-plan | High volumes, flexible terms | Investors must check delivery risk |

4. Risks & Watch-points

- Interest rate risk: Global monetary tightening could impact mortgage affordability.

- Oversupply in select sub-markets: Some peripheral communities are facing abundant units — exercise caution.

- Currency / geo-political headwinds: As always, offshore capital flows are sensitive to global sentiment.

5. Looking Ahead: Predictions for 2025-26

- Sales prices to rise a further 5-10% across core areas, with villas possibly touching 10-12%.

- Rental yields to stabilise or increase slightly as demand stays strong.

- Off-plan launches may shift towards value-centric units — 1- and 2-bed apartments with payment flexibility.

- Investors increasingly favour communities near transport nodes and lifestyle amenities.

Conclusion

For stakeholders in Dubai’s real-estate market — buyers, investors, landlords and tenants alike — Q1 2025 offers important signals. The underlying fundamentals remain robust, albeit not without risk. By staying informed and focusing on quality locations and product types, one can position wisely for the next phase of market evolution.